A strong cash flow is one of the most important factors in making your company successful, but that can create a serious challenge in some trade relationships.

Traditional finance methods for managing cash flow are often too expensive or inflexible for many businesses. Supply chain finance is an alternative finance method that provides short-term funding to improve your working capital.

This financing method protects the supply chains of medium-to-large Australian business by introducing a third party into the buyer-supplier relationship.

Let’s look in-depth at how supply chain finance works.

What is supply chain finance?

It’s an unfortunate reality of business that each party in a trade relationship often has conflicting goals. They’re each concerned with their own business’s cash flow however, which means the supplier wants their money quickly, while the buyer generally wants to postpone payment for as long as possible.

Introduce a complex supply chain like manufacturing or retail into the mix, where suppliers are also buyers, and the potential problems multiply.

Supply chain finance is a smart financing option that offers buyers and suppliers an opportunity to work together to stabilise both parties cash flows. It introduces a financial intermediary – a third party – into the buyer-supplier relationship.

Think of supply chain finance as an innovative hybrid of trade finance and debtor finance. The third-party financier almost immediately advances the money that the buyer owes to the supplier, ensuring that the supplier receives payment as soon as possible. They later recover that money from the buyer, allowing the business to benefit from longer payment terms.

As a result, the financier effectively stabilises the entire supply chain.

But how exactly does supply chain finance work?

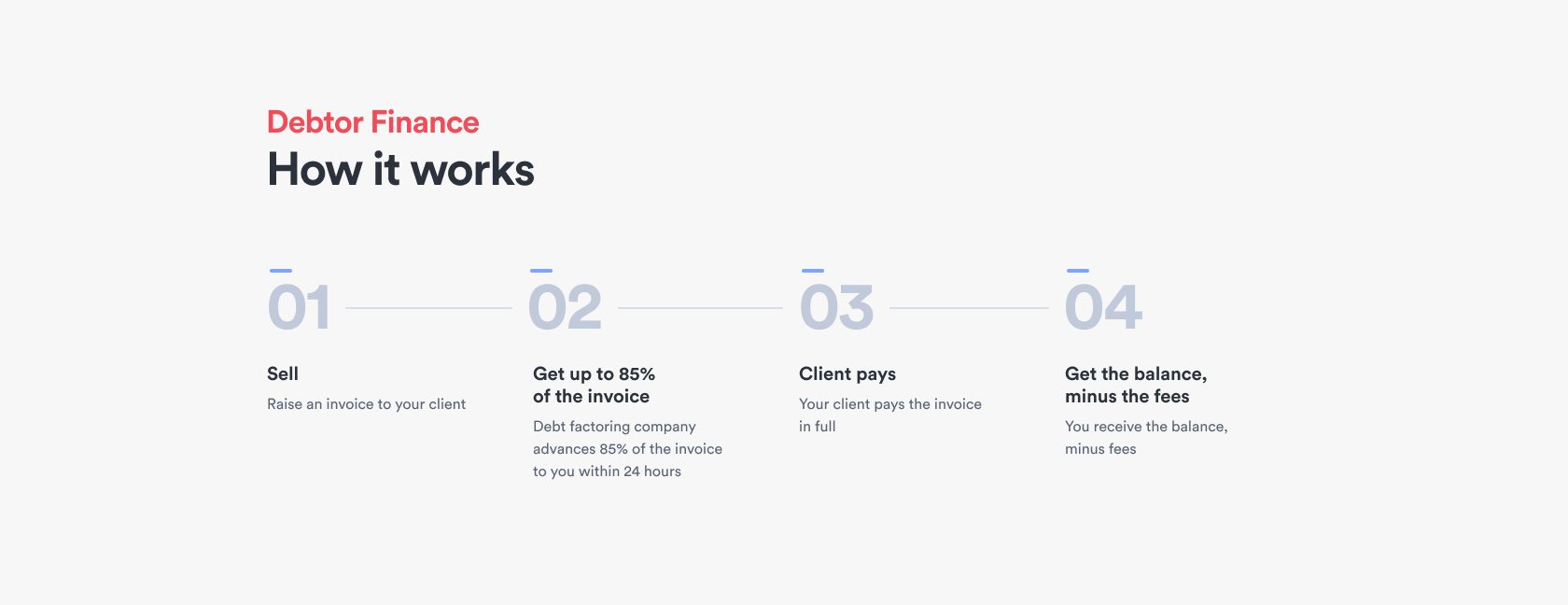

How the supply chain finance process works

The supply chain finance process is simple. It starts when the buyer enters into a supply chain finance agreement with a third-party financier. After this:

- The supplier invoices the buyer as normal

- The buyer approves the invoice as correct

- The supply chain financier pays the supplier soon after it’s approved

- The buyer then pays the financier up to 120 days later, as agreed by both parties

This means that the supplier doesn’t have to wait for the full payment term before they get their money. And that, in turn, means they can pay their own suppliers on time.

In short, the whole supply chain runs without cash flow bottlenecks.

Supply chain relationships are often uneven in terms of the power each party has in the transaction.

For example, larger buyers (such as big supermarket chains) can put smaller suppliers at risk of cash flow shortages by dictating longer payment terms. Meanwhile, small buyers may struggle with liquidity, and risk letting unpaid invoices fall overdue, which can then impact the entire supply chain – small, medium and large businesses alike.

Complex supply chains and global trading relationships can exacerbate the problems. Time delays with cross-border transactions or late payments can have a domino effect across the whole supply chain.

Supply chain finance can strengthen the entire chain for both buyers and suppliers.

How does supply chain finance help buyers?

Generally, the buyer is responsible for establishing supply chain finance. So why would they want to do that?

As a buyer, paying upfront for high-value goods or services can be a big hit to your cash flow. Using supply chain finance helps you to:

- save money by taking advantage of any early payment discounts

- still trade as usual with the cash you have available

- maintain a better relationship with your supplier, which strengthens the stability of your supply chain.

Additionally, a supply chain finance facility is also generally considered an ‘off-balance sheet’ source of funding, which means it doesn’t generally affect your ability to access other traditional funding sources, such as bank loans.

How does supply chain finance help suppliers?

As a supplier, using a supply chain finance facility means you:

- get paid earlier

- improve your balance sheet by lowering your accounts receivables

- can piggyback on a larger buyer’s credit rating, taking advantage of the favourable terms they’ve negotiated.

Put simply, supply chain finance has advantages for both suppliers and buyers, and reduces risk along the whole chain.

Octet’s Supply Chain Accelerate: a revolutionary working capital solution

We’ve designed our Supply Chain Accelerate solution to provide buyers with supply chain financing that they can then use with specific sellers.

Is Supply Chain Accelerate right for you?

Ideal buyer businesses are highly profitable with a larger turnover. To show this, you’ll need to provide a copy of your recent, audited financials, which we’ll check against our internal credit rating.

If you’re approved, here are just a few ways Supply Chain Accelerate can give your business a boost.

Quick setup

We have a fast setup process for both buyers and sellers. From the initial assessment to underwriting and on-boarding to go live, it typically only takes a few weeks.

Unsecured funding

Unlike more traditional financing, Supply Chain Accelerate is completely unsecured. That means we don’t require director or company guarantees. Instead, you secure all finance against your business performance.

Flexible finance

Supply Chain Accelerate doesn’t have to be your only finance source. Use it to supplement other existing or planned funding facilities. If you need extra finance to top-up on an existing loan, you can do that. And since we take on the liability to your supplier, it doesn’t sit on your balance sheet, so it won’t interfere with applying for other finance.

Global security

We vet both you and your suppliers against global banking standards. We also carry out all transactions securely, keeping your data safe and using anti-fraud technology. This level of security gives you extra peace-of-mind in your supply chain.

Increased visibility

Our secure platform enables you to track each critical step in the supply chain process – from procurement to payment, and from order to cash. The platform also stores and validates all essential documents at each stage, giving both buyer and supplier full transactional visibility.

Cost splitting

You can choose to pay the Supply Chain Accelerate cost yourself, have the other party pay it, or split it between both businesses.

How Octet’s Supply Chain Accelerate can grow your business

Supply Chain Accelerate recently helped a domestic fashion clothes supplier that had an outstanding ledger of $5 million. The company had one main buyer and a good credit rating, but cash flow bottlenecks were stopping them from growing their business.

A competitor had offered this client debtor finance of up to $2.5 million with an 80% advance rate. However, since the company was a good credit risk, Octet offered them the full $5 million finance at 100%.

We on-boarded their main buyer, and as soon as they were authorised, we funded the business 100% of the claimed amount, minus our transaction fee. The buyer then had 90 days to repay us, effectively giving them an extension of credit.

And since our funding was more than double the amount of our competitor’s, our client had the cash flow to effectively double their revenue within the next 12 months. As a result, their net profit after establishing the supply chain finance facility significantly increased.

Negotiate smarter

Supply chain finance can help you to improve your cash flow, strengthen your supply chain and power your business growth. But we also have a range of other finance solutions that may suit your needs.

Discover more about Supply Chain Accelerate or talk to us today to see which solution will work best for you.

The comments and views in this communication are those of the author as at the date of this post and are subject to change without notice. This communication should not be construed as advice and you should act using your own information and judgment. Whilst information has been obtained from and is based upon multiple sources the author believes to be reliable, we do not guarantee its accuracy and it may be incomplete or condensed.